Directive on Accounting Standards: GCG-8 Purchased Intangibles

States the Government of Canada’s accounting policies for purchased intangibles.

Date modified: 2024-07-11

Hierarchy

Note to reader

This document is part of the Appendix A of the Directive on Accounting Standards.

A. Primary PSAS reference

PSG-8 Purchased Intangibles

B. Effective date

April 1, 2023

C. Government of Canada Consolidated Financial Statements

- The Government of Canada (GC) is applying PSG-8 on a prospective basis.

D. Purpose and scope

- This guideline provides guidance on the recognition and measurement of purchased intangible assets.

- Purchased intangible assets include, but are not limited to:

- intellectual property including patents, trademarks, copyrights, and plant-breeding rights (IPSAS 31.17);

- licences and permits, such as those for hunting and fishing;

- broadcasting rights or licences (IPSAS 31.42);

- airway route or landing rights (IPSAS 31.42);

- import quotas or licences (IPSAS 31.42);

- acquired lists of contacts, users, customers;

- scientific or technical knowledge;

- processes;

- Purchased intangible assets do not include:

- software (accounted for under GC 3150 Tangible Capital Assets);

- intangibles developed by the government or are otherwise in the research or development stage (including where the government pays for intangibles to be developed by third parties); and

- monetary items or financial instruments.

E. Recognition

- Further to PSG-8, purchased intangibles are recognized as assets when they:

- are purchased in an exchange transaction (i.e., involving consideration) from an arm’s length third-party;

- meet the asset definition in PS 1000 Financial Statement Concepts and PS 3210 Assets, and the general recognition criteria in PS 1000;

- are identifiable; and

- have a per-item cost of greater than $10,000 or as described in GC 3150.02.

- A purchased intangible asset is identifiable if it either (IPSAS 31.19):

- is separable, i.e., it is capable of being separated or divided from the entity and sold, transferred, licensed, rented, or exchanged, either individually or together with a related contract, identifiable asset or liability, regardless of whether the entity intends to do so; or

- arises from binding arrangements (including rights from contract or other legal rights), regardless of whether those rights are transferrable or separable from the entity or from other rights and obligations.

F. Measurement

- Purchased intangible assets should be initially recognized at cost.

- Purchased intangible assets should be subsequently measured at cost less accumulated amortization and less any impairment adjustments.

G. Amortization

- A purchased intangible asset should be amortized on a systematic basis over its useful life.

- Specifically, the cost less the residual value should be amortized over the purchased intangible asset’s useful life (IPSAS 31.96).

- Residual value for a purchased intangible asset should be assumed to be zero, unless there is either (IPSAS 31.99):

- a commitment by a third party to acquire the asset at the end of its useful life; or

- an active market for the purchased intangible and it is probable the market will exist at the end of the purchased intangible’s useful life.

- The amortization method should reflect the pattern in which the asset’s future economic benefits are expected to be consumed. Where no pattern is evident, straight-line amortization may be used (IPSAS 31.99).

H. Impairment

- Once a purchased intangible is recognized as an asset, conditions should be monitored at each annual reporting date, at a minimum, for evidence that a write-down of the asset’s carrying value to its net realizable value is necessary.

- Conditions suggesting a write-down is required include where the purchased intangible asset no longer enables or contributes to the entity’s ability to provide future goods or services, achieve its mandate, generate future cash inflows or reduce future cash outflows.

- Similar to tangible capital assets, for a write-down of purchased intangible assets to occur, the condition(s) must be expected to be permanent, and the write-down should not be reversed.

I. Departmental Financial Statements

- Applies without additional policy choices or interpretation for Departmental Financial Statements.

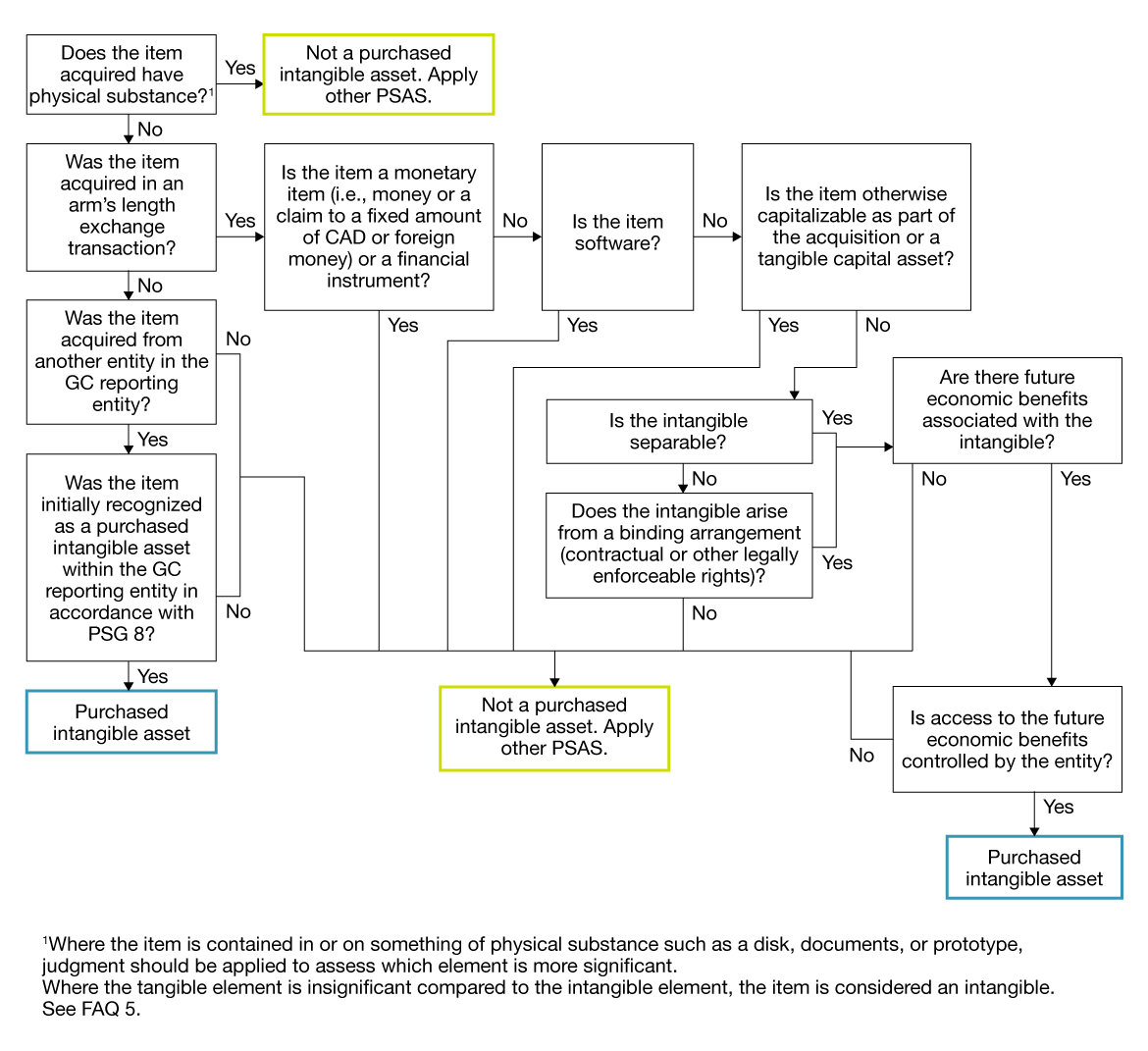

J. Flow chart for recognizing a purchased intangible under PSG-8

Flow chart - Text version

This figure illustrates some of the key questions that should be considered when determining if an item meets the definition of a purchased intangible asset.

- Does the item acquired have physical substance? There is a footnote to this question noting that, where the item is contained in or on something of physical substance, such as a disk, document or prototype, judgment should be applied to assess whether the physical or intangible element is more significant. Reference is made to FAQ 5 for further information.

- If yes, the item is not a purchased intangible asset.

- If no, continue to the following question.

- Was the item acquired in an arm’s length exchange transaction?

- If no, was the item acquired from another entity in the Government of Canada reporting entity?

- If no, the item is not a purchased intangible asset.

- If yes, was the item initially recognized as a purchased intangible asset within the GC reporting entity in accordance with PSG-8?

- If yes, the item is a purchased intangible asset.

- If no, the item is not a purchased intangible asset.

- If yes, continue to the following question.

- If no, was the item acquired from another entity in the Government of Canada reporting entity?

- Is the item a monetary item (i.e., money or claim to a fixed amount of CAD or foreign money) or a financial instrument?

- If yes, the item is not a purchased intangible asset.

- If no, continue to the following question.

- Is the item software?

- If yes, the item is not a purchased intangible asset.

- If no, continue to the following question.

- Is the item otherwise capitalizable as part of the acquisition of a tangible capital asset?

- If yes, the item is not a purchased intangible asset.

- If no, continue to the following question.

- Is the intangible separable?

- If no, does the intangible arise from a binding arrangement (contractual or other legally enforceable rights)?

- If no, the item is not a purchased intangible asset.

- If yes, continue to the following question.

- If yes, continue to the following question.

- If no, does the intangible arise from a binding arrangement (contractual or other legally enforceable rights)?

- Are there future economic benefits associated with the intangible?

- If no, the item is not a purchased intangible asset.

- If yes, is access to the future economic benefits controlled by the entity?

- If no, the item is not a purchased intangible asset.

- If yes, the item is a purchased intangible asset.

K. Other related references

- Frequently Asked Questions on the Guideline on Accounting for Purchased Intangibles (accessible only on the Government of Canada network).