Guide to Ex Gratia Payments, Honorariums and Gifts

Hierarchy

Archives

This guide replaces:

- Claims and Ex Gratia Payments, Guideline on [2018-05-29]

- Ex Gratia Payments and Honorariums, Guide to [2022-05-27]

1. Date of publication

This guide was published on November 22, 2019, and incorporates changes effective as of June 20, 2024.

This guide replaces the provisions on ex gratia payments in the Guideline on Claims and Ex Gratia Payments dated October 1, 2009.

2. Application, purpose and scope

This guide applies to the organizations listed in section 6 of the Policy on Financial Management.

The purpose of this guide is to support departments in managing ex gratia payments, honorariums and gifts.

This guide supports the requirements set out in Appendix A of the Treasury Board Directive on Payments and does not have any new mandatory requirements. Examples are provided for illustrative purposes only and may not apply to all departments or situations.

3. Overview of ex gratia payments

3.1 Definition

The Directive on Payments defines an “ex gratia payment” as follows:

A benevolent payment made by the Crown used only when there is no other statutory, regulatory or policy vehicle to make such a payment. The payment is made in the public interest for loss or expenditure incurred where the Crown has no obligation of any kind, no legal liability, and where the claimant has no right of payment and is not entitled to relief in any form.

3.2 Considerations for issuing an ex gratia payment

Ex gratia payments should be managed with prudence given that they closely resemble gifts. The following are key considerations for the use of ex gratia payments:

- ex gratia payments should be considered only in situations of loss or incurred expenditure

- ex gratia payments should be used only in exceptional or urgent circumstances

- ex gratia payments are not intended to be used as a mechanism to deliver a program and are not appropriate for making recurring payments

- the purpose for which the ex gratia payment is intended must fall within the mandate of the department

- an ex gratia payment cannot be used if there are any legal restrictions to doing so (for example, a department may be prevented from issuing payments for certain expenses, such as interest payments, in their enabling legislation)

- ex gratia payments should not be used to address claims or situations where a liability exists (refer to the Guide to Claims for more information)

3.3 Authorities for issuing an ex gratia payment

Table 1 details the various authorities available for issuing an ex gratia payment. When considering the use of an ex gratia payment, departmental chief financial officers should engage their legal services unit and can consult with the appropriate program sector at the Treasury Board of Canada Secretariat (TBS) and the Office of the Comptroller General to determine the appropriate authority.

| Authorities under which the issuance of an ex gratia payment may be considered | |||

|---|---|---|---|

| Directive on Payments | Ministerial authority | Treasury Board or Governor in Council | |

| Guidance on appropriate usage |

|

|

|

| Approval level required |

|

|

|

3.4 Considerations for issuing an ex gratia payment under the Directive on Payments

Proposed payment is not covered by another governing instrument

Under subsection A.2.2.3.1.1 of Appendix A of the Directive on Payments, managers must ensure that ex gratia payments are issued only when the proposed payments are not covered by other authorities, governing instruments, Treasury Board policies or other mechanisms for compensation. Examples of other authorities are program funding, transfer payments, statutory or regulatory schemes, insurance and contracts.

Before issuing an ex gratia payment, the delegated departmental manager must determine whether there are any other possible authorities for making the payment. If the proposed payment is covered by another governing instrument, the payment must be made pursuant to that instrument and not by means of an ex gratia payment.

For example, a consultant visited a departmental office for a meeting, and an employee accidentally placed several file folders on the consultant's eyeglasses and damaged them. The consultant asked the departmental manager for compensation to replace the damaged eyeglasses. The manager investigated the matter and determined that the damage was the result of an accident that occurred during the performance of the consultant's duties, and that the consultant's request for compensation should be treated as a claim (refer to section 4 the Guide to Claims for more information).

Proposed payment is not being used to fill a gap in another instrument

As part of the process to validate whether another governing instrument applies, managers must also ensure that ex gratia payments are issued only when they are not filling perceived gaps or compensating for the apparent limitations in another governing instrument, as required under subsection A.2.2.3.1.1 of Appendix A of the Directive on Payments.

In other words, if a particular situation is governed by another instrument and that instrument does not provide for the proposed payment, no ex gratia payment under the directive can be issued.

Similarly, ex gratia payments cannot be made under the Directive on Payments in employment contractual situations, including when a public servant’s effects are damaged, lost, stolen or destroyed.

3.5 Considerations for issuing an ex gratia payment under ministerial authority

As agents of the Crown, ministers may be able to exercise the Crown’s authority to authorize ex gratia payments in relation to matters falling within their mandates and outside the Treasury Board Directive on Payments.

When issuing an ex gratia payment under ministerial authority, the department’s chief financial officer should confirm that:

- the departmental legal services unit has determined that the proposed ex gratia payment falls within the department's mandate

- the Office of the Comptroller General has been consulted and has provided comments on applicable financial management policies and procedures

The minister should notify the President of the Treasury Board in writing when the ex gratia payment has been made. In this letter to the President, the minister should explain:

- why the ex gratia payment was made

- to whom it was made

- the amount and nature of the payment

3.6 Considerations for issuing an ex gratia payment under the authority of the Treasury Board or Governor in Council

The use of the following mechanisms outside the Treasury Board Directive on Payments should be assessed on a case-by-case basis:

- Treasury Board authority: the department may ask the Treasury Board to authorize the payment pursuant to the Ex gratia Payments Order, 1991, [(P.C. 1991-8/1695) September 1991] (see Appendix A of this guide) by means of a Treasury Board submission

- Governor in Council order: the department may seek authority for the payment through a specific Governor in Council order by means of a Governor in Council submission

The appropriate program sector at TBS should be consulted before and during the development of the Treasury Board submission or the Governor in Council submission for an ex gratia payment.

3.7 Determining the amount of an ex gratia payment

In determining an appropriate amount for an ex gratia payment, managers should consider the following:

- the underlying costs of amounts paid under comparable situations

- what is fair under the circumstances

- any contributing factors, including any actions or omissions by the potential recipient

The delegated departmental manager should also consider whether funds are available to the recipient from other reasonable means of compensation, such as:

- federal or provincial statutes

- private or public programs

- contract provisions

- commercial insurance or recovery from third parties

4. Overview of honorariums and gifts for First Nations, Inuit or Métis recipients

4.1 Definition

The Directive on Payments defines an honorarium for First Nations, Inuit or Métis recipients as follows:

A benevolent payment made by the Crown to First Nations, Inuit, or Métis recipients used only when there is no other statutory, regulatory or policy vehicle to make such a payment. The payment is made to a First Nations, Inuit or Métis recipient, who is not a government employee, to recognize or honour the collaborative efforts made by the recipient with respect to Indigenous ceremonies and other collaborative events or activities with the Government of Canada. The Payment can only be made where the Crown has no obligation of any kind, no legal liability, and where the recipient has no right of payment and is not entitled to compensation in any form.

4.2 Considerations for issuing honorariums and gifts for First Nations, Inuit or Métis recipients

Under the Treasury Board Directive on Payments, departments may issue honorariums or gifts to recognize or to honour the collaborative efforts made by First Nations, Inuit or Métis recipients.

Following are key considerations for the use of honorariums or gifts for First Nations, Inuit or Métis recipients. Honorariums and gifts:

- are not used if a service contract exists or would be more appropriate

- are not an entitlement, as there is no expectation of payment or gift in exchange for the service rendered

- are not recurring payments or gifts to the same individual

- are not used to address claims or situations where a liability exists

4.3 Honorariums for First Nations, Inuit or Métis recipients

Honorariums should be considered only after examining the appropriateness of proceeding with a service contract. A service contract should be established where there is an expectation that compensation will be provided for a service rendered even where the payment may be nominal. Service contracts should also be considered where there is an ongoing or recurring nature to the payment (for example, the same individual is receiving repeated payments). Departmental managers should consult their procurement functions to determine the appropriate form of contract.

Honorarium payments should always be gratuitous. The decision to provide an honorarium should have no influence on the decision of the individual to participate or volunteer their time. There is no legal obligation to make the payment, and the recipient has no legal right to the payment.

The underlying authority to issue honorarium payments can be found in the Ex gratia Payments Order, 1991 [(P.C. 1991-8/1695) September 1991] (Appendix A of this guide), which forms the basis for the Treasury Board Directive on Payments.

Departments should consider the appropriateness of each honorarium and the circumstances of each situation (see section 5 for further guidance). To the extent possible, departments are encouraged to restrict their delegation of financial authorities to require higher levels of approval for scenarios involving large-scale activities or exceptional circumstances in the context of their departmental mandate.

4.4 Gifts for First Nations, Inuit or Métis recipients

The underlying authority to issue gifts can be found in Order Authorizing the Provision of Gifts to First Nations, Inuit and Métis Elders (Appendix B of this guide) and the Treasury Board Directive on Payments.

The Order Authorizing the Provision of Gifts to First Nations, Inuit and Métis Elders authorizes deputy heads and chief executive officers (CEOs), whatever their title, of a department as defined in section 2 of the Financial Administration Act to transfer public property in the form of nominal non-monetary gifts to a First Nations, Inuit or Métis recipient.

4.4.1 Deputy head or chief executive officer approval

Deputy heads or CEOs must approve the giving of gifts. This approval can be given on a case-by-case basis or, in the case of gifts under $500, the approval could be more general and authorize the giving of gifts in certain circumstances or for particular events or activities.

If deputy heads or CEOs approve the giving of gifts, they may, as part of that approval, authorize departmental officials to provide the gifts in accordance with the parameters of the approval.

When deputy heads or CEOs authorize officials within the department to provide gifts within the approved parameters, the following are the key considerations:

- authorities should be assigned to positions identified by title and not to individuals identified by name

- individuals authorized to provide gifts cannot transfer these authorities to others

- the approval and authorization should be documented (may be included with the department’s delegation of authority documentation) and should include details related to the type of events and the associated gifts that are authorized

4.4.1.1 General approval

For gifts of $500 or less, the deputy head or CEO may periodically sign the approval or authority instrument (document) that sets out the parameters of the approval and the authority for departmental managers to provide the gifts within those parameters.

For example, a deputy head or CEO may annually designate certain departmental officials to provide gifts below $500 without returning to seek additional authorization in each instance during a given year.

4.4.1.2 Specific approval

For gifts over $500, deputy heads or CEOs are required to provide specific approval under the subsection A.2.2.1.4 of Appendix A in the Directive on Payments.

For example, in unique circumstances, departmental officials who wish to approve a gift valued at more than $500 will need to seek specific deputy head or CEO approval in each instance.

Departments should consider the appropriateness of each gift and the circumstances of each situation (see section 5 for further guidance).

4.4.1.3 Inclusion of sales taxes

The established $500 limit for gifts includes applicable taxes, such as the Goods and Services Tax / Harmonized Sales Tax (GST/HST) and Quebec Sales Tax (QST), when applicable. Delivery charges are not to be included in the threshold amount.

5. Appropriate honorariums or gifts

When deciding between honorariums and gifts and the related amounts, departments should adhere to the Treasury Board Directive on Payments and consider the individual recipient or recipient’s community preferences.

Departments should consider the circumstances and appropriateness of an honorarium or gift for each occurrence. In considering the appropriate use of honorariums and gifts, and to aim for consistent treatment of similar circumstances within the federal government, departments should take measures such as:

- consulting the Elder / Knowledge Keeper Protocol Guide produced by the Knowledge Circle for Indigenous Inclusion; to obtain further information, contact the Indigenous Cultures, Protocols and Accessibility Resource Center at crcapa-icparc@sac-isc.gc.ca

- restricting specific approval or delegation for scenarios that involve large-scale activities or exceptional circumstances in the context of the mandate of the department

Departments may also consult other departments and agencies that have subject matter expertise to inform the establishment of appropriate and consistent delegations and approvals from the deputy head or CEO. A list of current practices is available on GCpedia.

6. Choosing the right mechanism

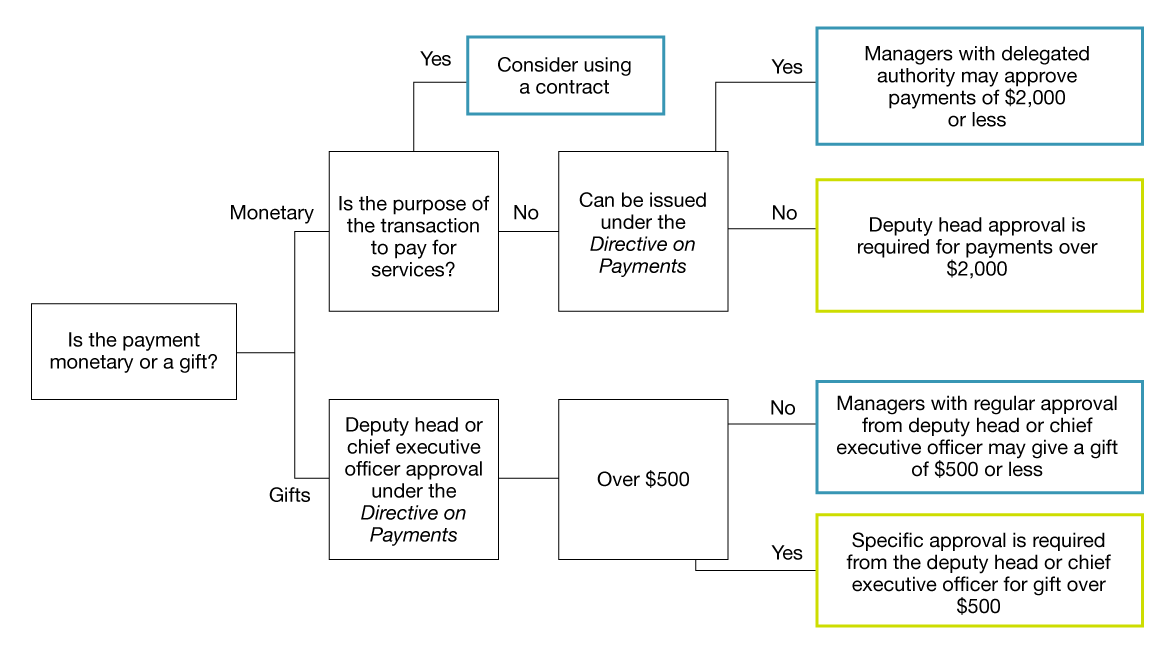

Figure 1 is a decision tree to help departments decide on the most appropriate honorariums or gifts and the required approval levels.

Figure 1 - Text version

Figure 1 shows a decision tree of questions to ask and steps to follow when processing a transaction for paying an honorarium or giving gift.

The first question to ask is whether the payment is monetary or a gift.

If the payment is monetary, the next question is whether the purpose of the transaction is to pay for services. If the answer is yes, consider using a contract. If the answer is no, then the amount can be issued under the Directive on Payments:

- managers with delegated authority may approve payments of $2,000 or less

- deputy head approval is required for payments over $2,000

If the payment will be a gift, then it requires deputy head or chief executive officer approval under the Directive on Payments:

- managers with regular approval from the deputy head or chief executive officer may give a gift of $500 or less

- specific approval is required from the deputy head or chief executive officer for a gift over $500

7. Other honorarium payments and gifts

The authority to issue other honorarium payments and gifts may be found in program legislation or departmental legislation, or in some other special approval such as an order-in-council. Departmental managers may want to consult with their legal services unit to ascertain the authority to issue honorarium payments and gifts.

8. Reporting

Honorariums and gifts that total over $500 to an individual recipient may incur a tax liability. The department will report total amounts on the appropriate tax slip at year-end in accordance with the Income Tax Act.

All ex gratia payments and honorariums or gifts for First Nations, Inuit or Métis recipients are to be reported in the Public Accounts of Canada in the fiscal year when they were issued to the recipient, in accordance with the Receiver General Manual, “Public Accounts of Canada Instructions.” Information about publication exemptions will be provided to departments in the Receiver General Manual or through other communication from the Office of the Comptroller General.

9. References

Legislation

Related policy instruments

Other

- Employers’ Guide: Payroll Deductions and Remittances

- Ex gratia Payments Order, 1991 [(P.C. 1991-8/1695) September 1991]

- R105 Regulation 105 Waiver Application form

- Receiver General Manual

10. Enquiries

Members of the public may contact Treasury Board of Canada Secretariat Public Enquiries if they have questions about this guide.

Individuals from departments should contact their departmental financial policy group if they have questions about this guide.

Individuals from the departmental financial policy group may email Financial Management Enquiries at fin-www@tbs-sct.gc.ca for interpretation of this guide.

Individuals from departments and agencies may also contact the Knowledge Circle for Indigenous Inclusion on matters of protocol at crcapa-icparc@sac-isc.gc.ca).

Appendix A: Ex gratia Payments Order, 1991 [(P.C. 1991-8/1695) September 1991]

P.C. 1991-8/1695

September 5, 1991

His Excellency the Governor General In Council, on the recommendation of the Treasury Board, is pleased hereby to revoke the Ex gratia Payments Order, 1974, made by Order in Council P.C. 1974-4/1946 of September 3, 1974, and to make the annexed Order(1) respecting ex gratia payments, 1991, in substitution therefor.

(1) Order respecting ex gratia payments, 1991

Short Title

1. This Order may be cited as the Ex gratia Payments Order, 1991.

Authorization

2. The Treasury Board may authorize any ex gratia payment.

3. The Treasury Board may designate the deputy head of any department or departmental corporation named in Schedule I or II to the Financial Administration Act or of any other division or branch of the public service of Canada, including a commission appointed under the Inquiries Act, that is designated by the Governor in Council as a department for the purposes of the Act, and the Judge Advocate General, to authorize ex gratia payments.

4. The Treasury Board may authorize any deputy head designated pursuant to section 3 to designate an employee of the deputy head's department, division or branch to authorize ex gratia payments on the deputy head's behalf.

Appendix B: Order Authorizing the Provision of Gifts to First Nations, Inuit and Métis Elders

June 21, 2024

Confidence of the King’s Privy Council

Whereas the Government of Canada, in achieving reconciliation, is committed to undertaking a distinctions-based approach by respecting the cultures and protocols of First Nations, Inuit and Métis when it takes part in collaborative ceremonies, events or activities involving First Nations, Inuit or Métis;

Therefore, Her Excellency the Governor General in Council, on the recommendation of the President of the Treasury Board and the Treasury Board, under subsection 61(2) of the Financial Administration Act, in support of the Government of Canada’s initiatives in relation to reconciliation, authorizes a deputy head or a chief executive officer — whatever their title — of a department, as defined in section 2 of that Act, to transfer public property, in accordance with the Treasury Board’s Directive on Payments, in the form of nominal non-monetary gifts to a First Nations, Inuit or Métis recipient, as that term is defined in that Directive, who is involved in a collaborative ceremony, event or activity in which the Government of Canada takes part, to recognize or to honour the collaborative efforts made by that recipient’s community.